As we step into February 2026, Australia’s climate reporting landscape has officially entered a new phase. Group 1 entities—our largest listed companies and financial institutions—have now been operating under mandatory AASB S1 and S2 requirements since 1 January 2025, while Group 2 entities are counting down to their 1 July 2026 commencement date. For those of us working at the intersection of climate reporting and assurance, this is no longer a preparation exercise—it’s implementation reality.

This opening post of 2026 captures the key regulatory developments that have emerged since late 2025, focusing on assurance standards, disclosure proportionality, and the tools being developed to support practitioners and preparers alike.

The Deep Dive: Key Developments

1. AUASB Issues ASSA 2025-10: Assurance on Voluntary Sustainability Reports

Source: AUASB – ASSA 2025-10 (21 January 2026)

In a significant move, the Auditing and Assurance Standards Board (AUASB) has issued ASSA 2025-10, which establishes the phasing in of assurance requirements for Group 1, 2 and 3 entities preparing voluntary sustainability reports under the Corporations Act 2001.

Key Points:

- The standard bridges the gap between mandatory and voluntary reporting regimes

- Provides clarity for entities that wish to obtain assurance on sustainability reports before their mandatory commencement date

- Aligns the assurance framework with the broader ASSA 5000 suite

Practitioner Note: This is particularly relevant for Group 2 and 3 entities wanting to “dry run” their sustainability reports with assurance before mandatory requirements kick in.

2. AASB S2 Scenario Analysis Workshops – March 2026

Source: AASB Reporting Roundup December 2025 (17 December 2025)

The Australian Accounting Standards Board has announced AASB S2 Scenario Analysis Workshops scheduled for March 2026. This is a direct response to one of the most challenging requirements of AASB S2: the climate-related scenario analysis.

Why This Matters:

- Scenario analysis under AASB S2 requires entities to assess climate resilience under different futures (including a 1.5°C pathway)

- Many preparers have flagged this as a significant capability gap

- The AASB’s workshops signal recognition that hands-on guidance is needed beyond written standards

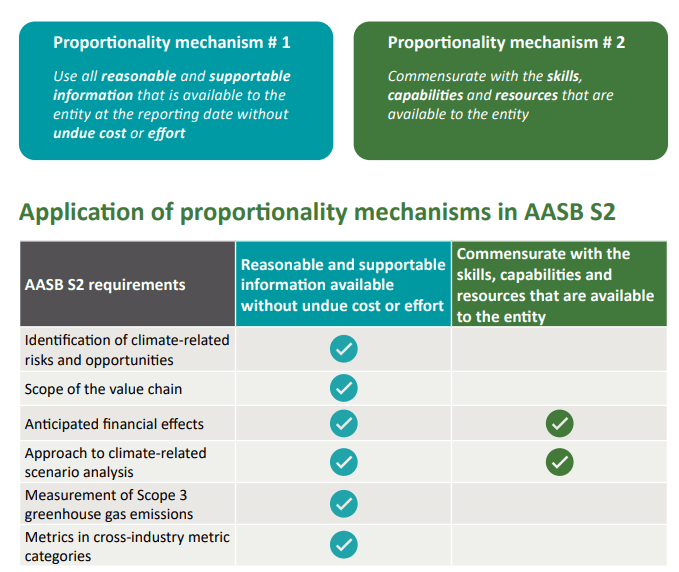

3. Proportionality Mechanisms in AASB S2

Source: AASB – Proportionality Mechanisms in AASB S2 (9 September 2025)

The AASB has published guidance on proportionality mechanisms embedded within AASB S2. These mechanisms are designed to support disclosures involving significant judgement or uncertainties.

Key Proportionality Features:

- Allowance for qualitative disclosures where quantification is not yet feasible

- Recognition that smaller entities (within Group 1) may have less sophisticated data systems

- Emphasis on “reasonable and supportable” information rather than perfect precision

Practitioner Note: This guidance is essential reading for auditors and preparers navigating the first year of mandatory reporting.

4. Safeguard Mechanism: 2024-25 Compliance Cycle Complete

Source: Clean Energy Regulator – Safeguard Mechanism

The Safeguard Mechanism continues to operate in parallel to the sustainability reporting regime. With the 2024-25 compliance cycle now complete:

- 135.9 million tonnes CO2-e covered emissions reported

- 7.3 million ACCUs surrendered

- 1.4 million SMCs surrendered

Looking Ahead: The CER’s Unit and Certificate Registry is now the single source of truth for ACCU and SMC holdings.

Practical Takeaway: What to Do in February 2026

- For Group 1 Entities: Your first mandatory sustainability reports are due with your next annual report. Ensure your scenario analysis methodology is documented and defensible. Consider attending the AASB S2 workshops in March.

- For Group 2 Entities (July 2026 start): Now is the time to conduct a gap analysis against AASB S1/S2. Consider voluntary assurance under ASSA 2025-10 as a practice run.

- For Assurance Practitioners: Familiarise yourself with ASSA 2025-10 and the illustrative auditor’s reports under ASSA 5000.

- For Safeguard Facilities: Verify your ANREU/Registry holdings before the SMC application window closes.

Sources

- AUASB: ASSA 2025-10 – Assurance on Voluntary Sustainability Reports – 21 January 2026

- AASB: Reporting Roundup December Edition – 17 December 2025

- AASB: Proportionality Mechanisms in AASB S2 – 9 September 2025

- CER: Safeguard Mechanism Overview – Accessed February 2026