In September 2025, the AASB published a guidance note titled “Proportionality Mechanisms in AASB S2” (9 September), clarifying how entities should apply judgement so that climate disclosures are scaled sensibly to size, complexity, and capacity.

This move helps signal that while the standard is mandatory in scope, not every disclosure has to be equally elaborate.

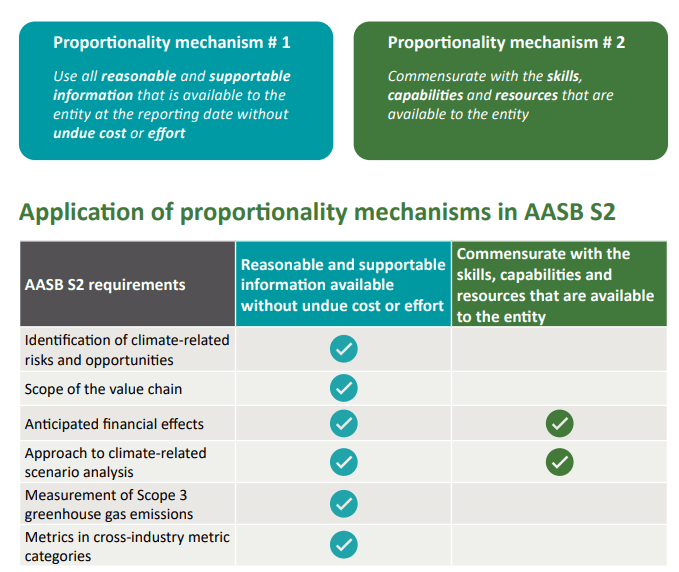

What the proportionality guidance says (in practice)

- The mechanisms allow entities to use reasonable and supportable information available at the reporting date — without undue cost or effort. (ESG Broadcast)

- Entities can adopt more scaled-back approaches in areas like scenario analysis, methodologies, or quantification when full technical work is impracticable given their resources. (ESG Broadcast)

- Importantly, proportionality does not remove disclosure obligations. Entities must still meet all core objectives of AASB S2, but can manage how deeply or quantitatively to go in each section. (ESG Broadcast)

- The guidance identifies which parts of the standard are more amenable to proportional judgment (governance, risk identification, value-chain scoping, financial effect estimates, scenario work). (ESG Broadcast)

This clarification is a strong signal: the Board expects flexibility, but wants clear documentation of judgments, method limitations, and rationale.

Why this matters (especially for smaller or mid-tier entities)

- Many organisations fear that compliance with S2 will require heavy modeling, climate science expertise, or third-party consultants. The proportionality guidance offers breathing room.

- It helps bridge a capability gap: firms with limited data, technical staff, or budget can still comply meaningfully without being penalised for not doing everything at “Big 4 level.”

- The guidance supports the phased rollout to Group 2 and 3 reporters in 2026–27 by setting expectations of scalability rather than uniformity.

- However, the flipside: those who adopt minimal disclosures too early risk being judged harshly by auditors, regulators, or stakeholders if their rationale is opaque.

What preparers and auditors should do now

- Map out which portions of S2 you will scale back (e.g. limited scenario modelling, qualitative risk impact descriptions) and document why you adopted those choices.

- Use the proportionality guidance to defend judgment calls if auditors query your methodological shortcuts.

- Don’t over-simplify: even scaled disclosures must still respond to all four pillars (governance, strategy, risk management, metrics/targets).

- Prepare for future benchmarking: as more entities disclose, the bar for minimal acceptable practice will evolve, so build your disclosure capability progressively.

- Audit teams should treat proportional disclosures as red-flag areas — check whether the judgment is defensible, transparent, and consistent with your entity’s context.

Closing (my take)

This proportionality guidance is a smart, necessary balancing act. It signals that AASB expects inclusivity — letting smaller or less sophisticated entities comply in ways that match their capacity — while preserving the core disclosure goals.

However, not all practitioners will interpret “proportionate” the same way. The real test will lie in assurance practice, regulator reviews, and peer benchmarking. In my upcoming research, I’ll be watching how proportionality is implemented, challenged, and rationalised — especially where scaled approaches verge on minimalism.

📘 Source: AASB Proportionality Mechanisms in AASB S2 (9 Sept 2025) (AASB)

Additional contextual reporting framework: KPMG’s summary of Australia’s sustainability reporting regime (KPMG)